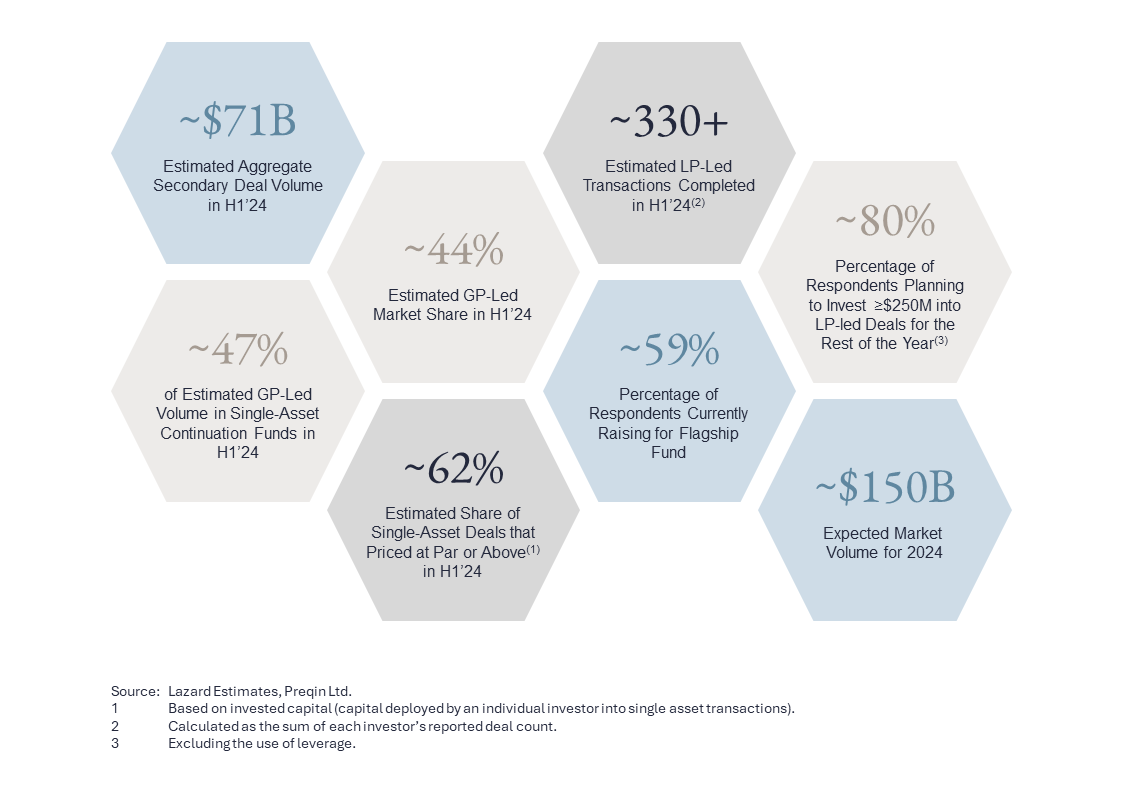

Key Report Findings

- The secondary market had a strong start in H1’24 and is anticipated to surpass its 2023 performance, with continued growth expected in the forthcoming years

- A surge in GP-led and LP-led deals is forecasted to persist in H2’24, propelled by the emergence of new capital sources, including specialist investors and increasing ’40 Act funds AUM

- Despite an anticipated increase in M&A and IPO activities, secondary deal volume is expected to remain robust going forward given GP’s and LP’s increasing predisposition to actively manage their portfolios

Six Predictions for the H2 2024

- Record-breaking market volume in FY 2024 given strong H1’24 performance

- Accelerating GP-led transaction volume in H2’24 driven by demand for continuation funds, particularly for Single-Asset transactions

- Bid-ask spreads will continue to narrow as buyside appetite grows and new entrants ramp up deployment pace, assuming recession risk recedes

- Increased breadth of LP-led transactions involving traditional funds, secondary funds, co-investment portfolios and management fund opportunities

- More traditional sponsors to expand their strategies to include GP-led teams, with a focus on Single-Asset continuation funds

- ’40 Act funds will put significant upward pressure on certain fund portfolios given increasing monthly inflows and the need to rapidly deploy that capital

Source: Lazard Estimates.